Knowing how to build credit is the key to unlocking a lifetime of financial privileges, from reduced interest rates, better borrowing options, reduced insurance costs, and easier approval for housing and employment.

In this post, we'll take you through every aspect of building credit, from how credit works to strategies you can use today to unlock the next level in your credit journey.

What is credit and why does it matter?

Credit is effectively your track record of borrowing money and paying it back, which shows to lenders how reliable you are when it comes to managing your debt commitments.

Credit is understood in the context of credit scores, which range from 300 (very bad) to 850 (perfect). Every individual who has any history of using some form of credit, be it a credit card, loan, etc, has a credit score attached to their name and social security number.

This said, credit matters because it can be the sole factor for determining your position in any credit situation. If you have bad credit, you may experience the following:

- Being denied

- Paying higher interest rates

- Fewer borrowing options

If your credit score is good, you can save lots of money on interest and unlock new borrowing, housing, and employment opportunities.

Understanding your credit score

Your credit score is a number between 300 to 850 that paints a picture to lenders for how "risky" it is to loan you money.

Every time you make a payment on a tradeline, a record is generally sent to the 3 main credit bureaus: Equifax, Experian, and TransUnion. These three bureaus gather and maintain your credit information. Lenders and scoring companies, like FICO, then use this information to generate your credit score when you apply for credit.

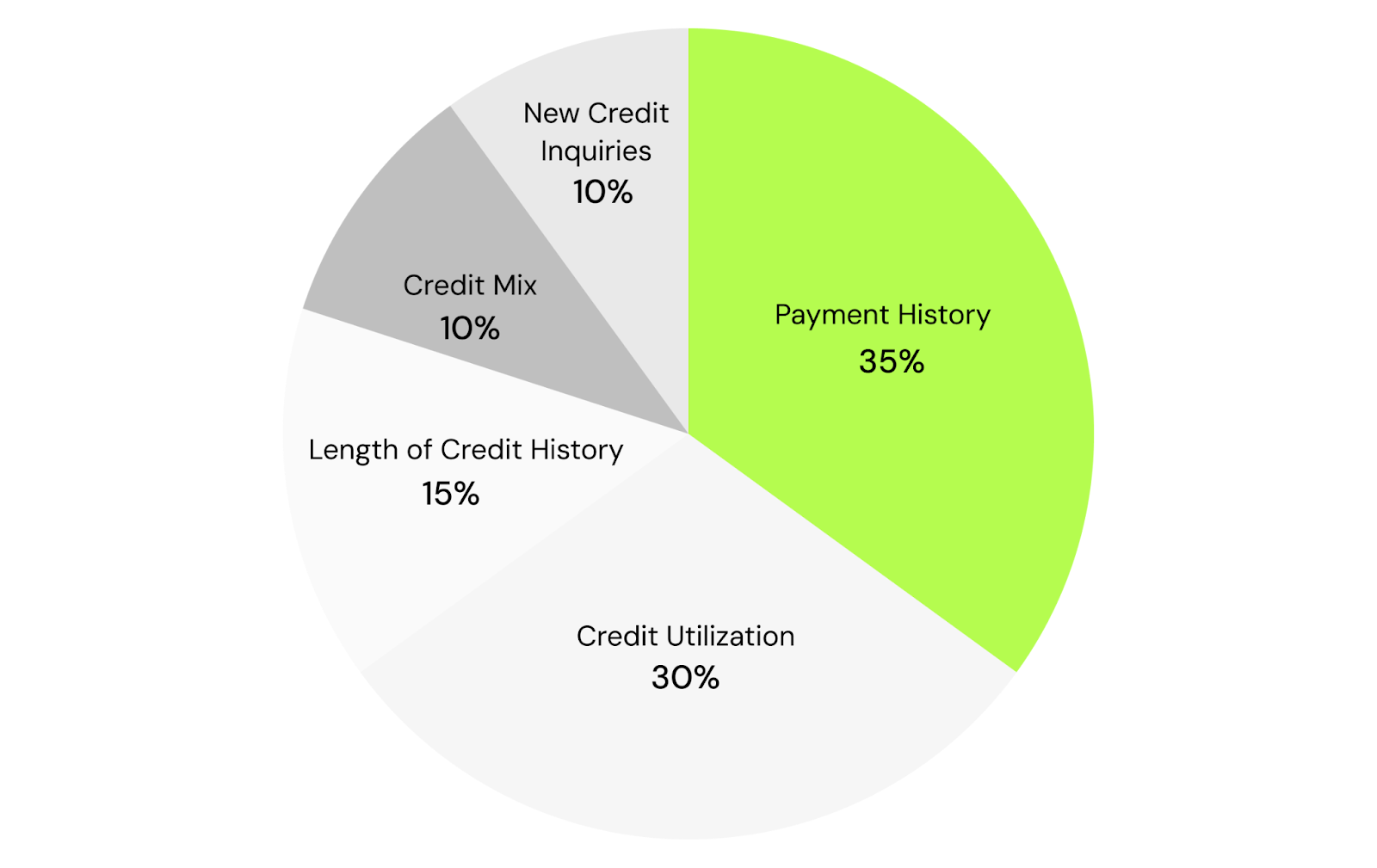

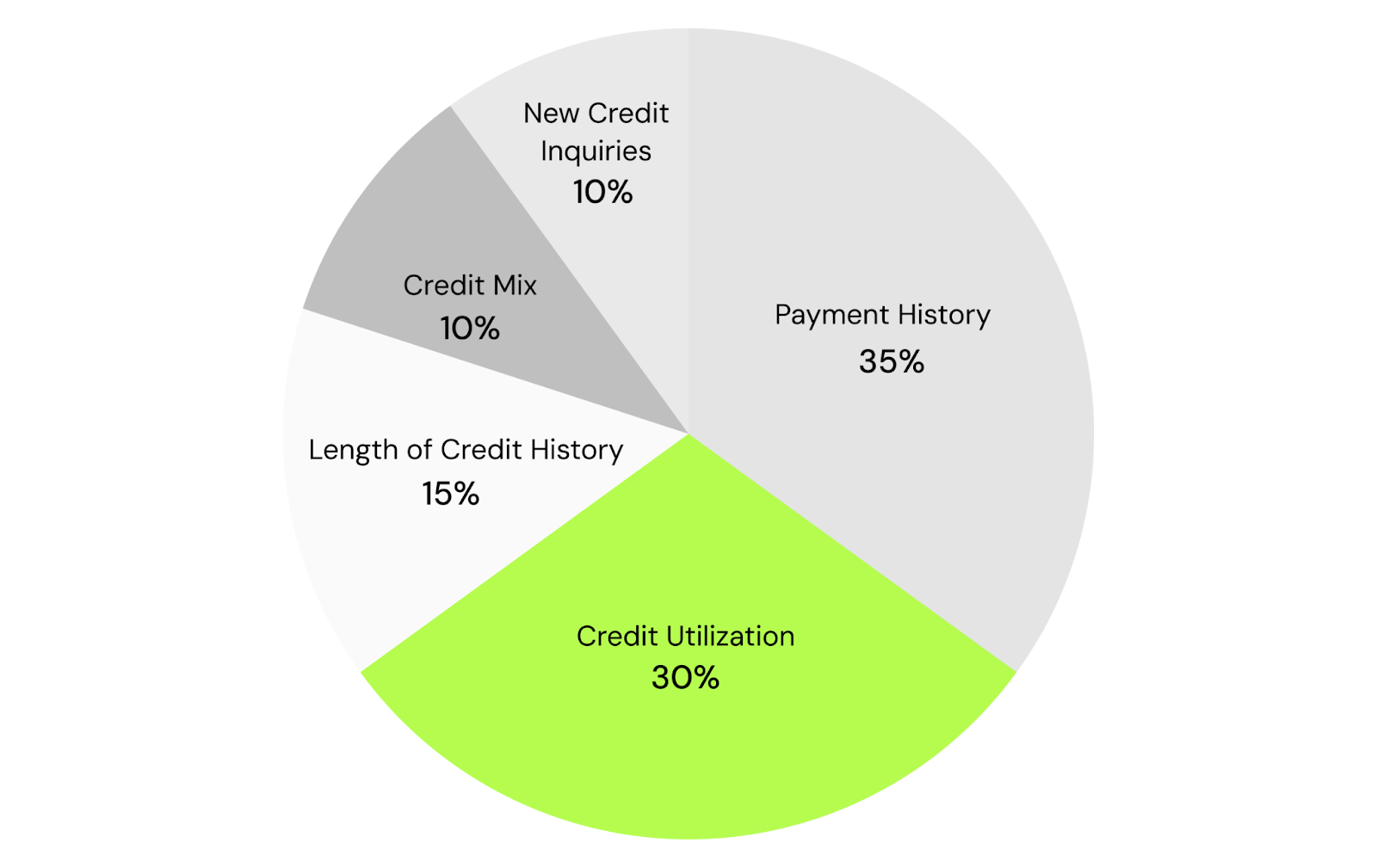

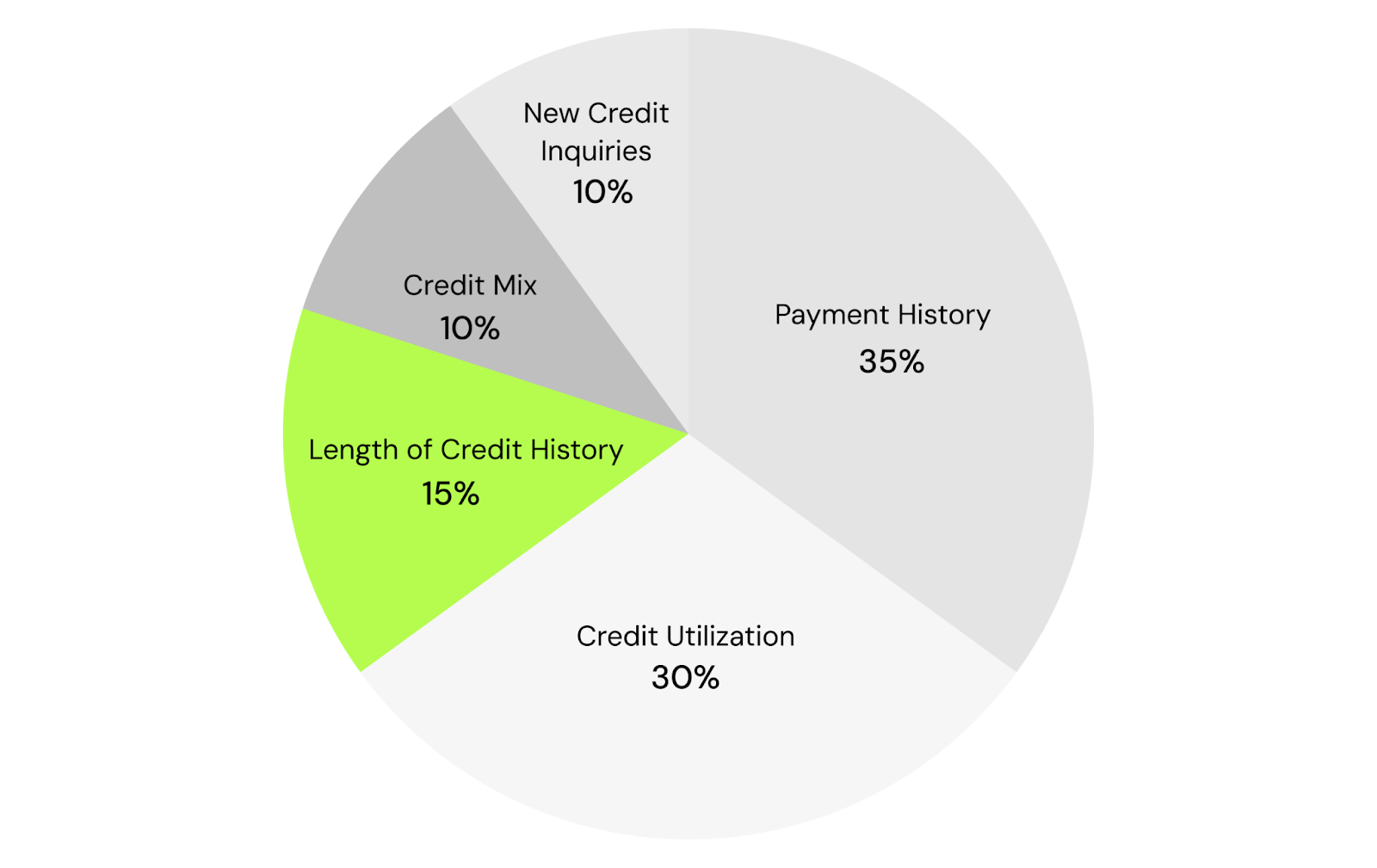

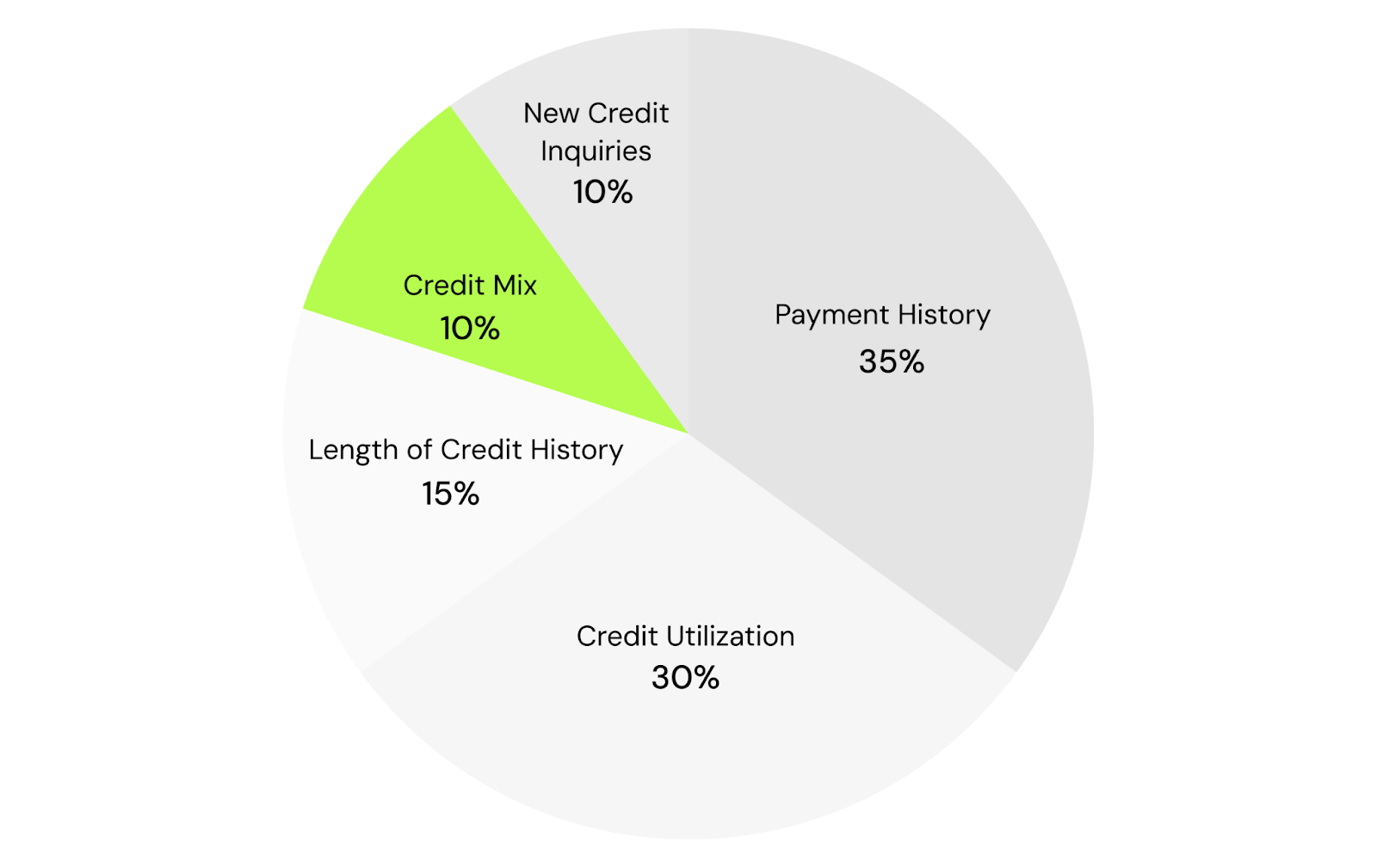

Your credit score is generally calculated by a mix of 5 factors derived from your past credit history: payment history, credit utilization, length of credit history, credit mix, and new credit inquiries.[1]

A credit-builder like Kikoff makes it easy to build credit, fast by giving users access to a Kikoff tradeline that's designed to target key credit factors while reporting to all three credit bureaus.

Let's jump in.

The five factors that determine your credit score

Payment history (35%)

Payment history is the single most important factor in determining your credit score.[1]

This factor answers one question lenders care most about, "do you pay your bills on time?"

Payment history looks at whether each agreed payment was made on time, was late, or unpaid at all across all reported accounts, including:

- Credit cards

- Loans (auto, personal, student, mortgage)

- Credit-builder or installment accounts

- Collections tied to credit accounts

Credit utilization (30%)

Credit utilization measures how much of your available revolving credit you're using.

Credit utilization mainly references revolving lines of credit, such as:

- Credit cards

- Department store cards

- Gas cards

- Secure Cards

Basically any credit line that renews or resets periodically.

Utilization is measured as a percentage, so if you have a credit limit of $1,000, and you spend $100, that is a 10% credit utilization.

It is generally established that keeping your credit utilization below 30% shows good credit utilization, and exceeding that 30% can damage your credit score.[2]

Length of credit history (15%)

Length of credit history is an indication of, on average, how long you've been using credit.

While this isn't as impactful as credit utilization or payment history, this does set a ceiling for how high your credit score can go.

If you have a longer credit history, that is generally a positive signal, as opposed to a short credit history where lenders can't observe your payment behavior over long periods of time.

Length of credit history is calculated mainly based on your oldest credit account, though the average age of your accounts is also considered. So if you have 3 credit cards, one opened 4 years ago, one 7 years ago, and one last year, your length of credit history is 4 years:

(4 + 1 + 7)/3 = 4

Keeping your oldest accounts open can help maintain a stronger credit history.

Credit mix (10%)

Credit mix is a measure of the variety of credit types you've managed.

If you've managed only credit cards, this is seen as a weaker credit mix than someone who has managed both credit cards and auto loans.

These are the general categories of credit that make up any individual's credit mix:

- Credit cards

- Auto loans

- Personal loans

- Student loans

- Mortgages

- Credit-builder or installment-builder loans

New credit inquiries (10%)

"New credit inquiries" refers to how often you apply for new credit with a hard inquiry.

You'll generally see a new inquiry on your report when you apply for:

- A new credit card

- An auto loan

- Finance accounts like a cell phone, furniture or other large purchases

Hard inquiries, a smaller factor, making up ~10% of your credit score should only be reported for 2 years and impact you for 1 year.[4]

On the contrary, soft inquiries do not affect the "new credit inquiries" factor and can be pursued without worrying about affecting credit, such as:

- Checking your own credit

- Pre-qualification checks

- Background checks

- Employer credit checks

- Account reviews by existing lenders

- Credit limit increases

- Better terms on existing lines of credit

Don't forget, Kikoff addresses the key factors that credit bureaus use to determine your credit score, and it's easy to sign up.

Now that we've gone over all 5 factors that determine your credit score, let's jump into how lenders actually get your credit score.

FICO vs. VantageScore: what's the difference?

FICO and VantageScore are the two primary algorithms used by lenders, banks, credit apps, and more, to calculate a user's credit score.

FICO is the original credit score, which is used by the vendors you'll most likely be applying for credit with, such as banks, credit cards, etc.

VantageScore is a more recent calculation, which is primarily used by websites and services that let you analyze your credit score quickly.

Both credit scores paint a similar picture of your credit, but there are slight variations in how they calculate it.

Here's a breakdown more specifically of how each score uses the 5 credit score factors:

| Credit Factor | FICO Weight | VantageScore Weight |

|---|---|---|

| Payment History | 35% | 40% |

| Credit Utilization | 30% | 20% |

| Length of Credit History | 15% | 21% |

| Credit Mix | 10% | 11% |

| New Credit | 10% | 8% |

What is a good credit score in 2026?

Although interest rate fluctuations in 2026 can affect your credit to a degree, a good credit score to aim for in 2026 is still above 740 for FICO, and 781 for VantageScore.

Maintaining above 740 FICO and 781 VantageScore will give you the best foundation for applying for loans, negotiating rates, and more.

What is a decent credit score in 2026?

A decent credit score in 2026 typically falls between 620 and 679 for FICO, and 661 to 780 for VantageScore.

Scores in this range show lenders that you are a moderate credit risk. While you can still access credit, you may face higher interest rates or less favorable loan terms compared with those who have higher scores.

How to build credit with a credit card

Whether you have a long credit history, or you're just starting out your credit journey, using credit cards in a smart, careful way can be a huge boost to your credit.

Start with a secured credit card

If you're just starting to build credit, secured cards are fantastic ways to get that jump on your credit score early.

Secured cards are credit cards that allow you to deposit cash into them, which becomes your credit limit, and as you make purchases on the card, those purchases get reported to the 3 credit bureaus (Equifax, Experian, and TransUnion).

This means you can build credit without the risk of managing a credit line you can't already afford, and virtually anyone can sign up for one. To learn about building credit with the Kikoff Secured Credit Card, click here.

Apply for a student credit card

If you're a student or young adult just starting out your credit journey, student credit cards are also a fantastic way to establish that first bit of positive credit history.

These are legitimate credit cards with a standard credit line, and usually have low limits. This said, they are very easy to get approved for, and are a fantastic option if you're starting out and don't want to have to fund a secured card.

Become an authorized user

If you have someone in your family who has good credit habits and access to credit cards, becoming an authorized user on at least one of their cards will spread the benefits of their spending to your credit score.

This can be risky, however, if you don't fully trust that the person who owns the card has good payment history and utilization, because if that person misses a payment or over-utilizes the card, it will negatively impact your credit score as well.

But if it's say a parent who is willing to add you as an authorized user, this tactic can have a positive impact on your credit score and help you build credit early as well as recover from bad credit. You don't even need a card or to see the account details, because what matters is being on a healthy, old account that reports to all three bureaus.

Graduate to an unsecured card

If you're ready to move on from the beginner strategies above, getting approved for a standard credit card is a super powerful way to build your credit.

Provided you're adhering to the best practices surrounding the 5 factors that impact credit scores above, building credit history on a standard unsecured credit card can skyrocket your credit in the long run.

Alternative ways to build credit

If you're looking to mix up your credit accounts and explore alternative credit building options, here are a few more solid ways to build credit:

Get a credit-builder loan

Credit-builder loans (CBLs) are small loans that serve the primary purpose of building the borrower's credit.

Typically, the lender of the CBL will take your deposit and put it in a locked savings account. You'll make monthly payments to the lender, and once the payments are done, you'll receive the final amount back, and each payment will have been reported to the 3 credit bureaus as positive payment history.

Report your rent payments

Rent is the highest expense for Americans, so utilizing that rent history to build your credit can be a no-brainer.

This can be fantastic since rent payments are quite large compared to typical monthly credit card expenses, which can show a significant impact on the payment history factor of your credit score.

As long as you are paying your rent on time, rent reporting is a great way to build credit.

Luckily, many apps exist now that will submit your rent payments to all 3 bureaus on your behalf, so find an app that suits you to unlock this easy credit win.

Add utility and subscription bills to your credit report

If you have a thin credit profile, using services to report utility and subscription bills is a great low-risk way to build credit.

This is ideal for new credit users, though impact can be limited as a result.

Take out a small personal or auto loan

If you feel ready to borrow responsibly, taking out a small personal loan or an auto loan can have a sizable positive impact on your credit score.

Just make sure you budget carefully and make your payments on time, since having missed payments on one of these loans will harm your credit score.

Use a cosigner to get approved for a loan or card

Similar to the strategy of becoming an authorized user on a family member's credit card, you can build credit by getting a cosigner to get approved for a loan or a credit card.

This allows you to jump through the hurdles of having a lower credit score if the person who is cosigning for you has a good credit score.

If you are able to find someone, be it a family member or close friend, ensure you are diligent to payback the loan or credit card statement on time. If you don't, your cosigner will see a drop in their credit score.

Common credit-building mistakes to avoid

Now that we've gone over all of the essentials of how to build credit, let's discuss some common mistakes beginners make.

If you avoid these mistakes and adhere to the principles in the 5 factors listed earlier, you'll be well on your way to a healthy credit score.

Paying late

New late payments will cause your score to nose-dive, not to mention send the message to potential lenders that you may not prioritize your finances and are more of a risk.

Other effects from paying late could be interest rate increases and other adverse action from your creditors.

If you're falling behind, be proactive and contact the creditor, they likely have hardship programs that can defer payments while keeping your reports in good shape.

Only paying the minimum

Many people will decide to only pay the minimum required payment on their credit card bill.

From a credit building perspective, it can initially feel like a safe, low cost way to keep an edge on your payment history.

However, only paying the minimum causes debt causes 2 problems:

- Your credit debt will skyrocket over time due to interest accumulation

- Your credit utilization rate will be way too high, thus damaging your credit

This said, it's recommended that you pay the entire statement balance as often as possible to avoid these pitfalls.

Maxing out your credit limit

Maxing out your credit limit on your credit cards may seem like a decent way to afford a big purchase in the short term, but doing so causes a few critical issues:

- This sends a "financial stress" signal to lenders

- This severely hurts your credit utilization rate

- Temporarily maxing out your card can immediately drop your credit score

In general, always try to keep your credit card utilization rate below 30%.[2]

Applying for too many accounts at once

Applying for several credit cards at once can seem appealing if you want to snatch those sign-on bonuses.

However, each application requires the lender to do a hard inquiry, each of which can hurt your credit score. If hard inquiries pile up in a short period of time, you'll see a hefty dent to your credit score.

To avoid this, try to space out your credit card applications 3-6 months from each other.

Closing old accounts

Closing old credit accounts can feel like a clean-up activity, but in reality, you're eliminating a vital part of your credit snapshot.

Length of credit history is a core factor in determining your credit score (the longer the better). By keeping old accounts open that are paid off, you're allowing those old accounts to help your credit history look longer to lenders, thus sending a positive signal.

Instead of closing old accounts, occasionally use them to prevent them from closing, pay them off immediately, and you'll be in a better spot.

Ignoring your credit report

Credit reports can be overwhelming, we get it.

However, it's very important to keep an eye on your credit report. Sometimes, errors take place, or fraud occurs, and if you don't check up on your credit report, you won't know to take action on these issues.

Check out this post on how to dispute credit report errors quickly and easily. Or, with a Kikoff plan, users can dispute errors on their credit report and send them to Equifax for review.

How long does it take to build credit?

The time it takes to build credit depends on your background. Let's take a look at a few hypothetical timelines for different scenarios, given healthy approaches to the 5 determining factors:

Timeline for building credit from scratch

- Months 1–2: During these months, open your first credit account (secured card, starter card, credit-builder loan, or authorized user). You probably won't have a FICO score yet, but this is where you'll start making on-time payments and keeping balances very low.

- Months 3–6: During this period, your credit score report will be generated, and you'll start to see more regular improvements, though your score is still fragile and can be severely damaged by any mistakes made.

- Months 6–12: Here, your positive payment history has noticeable data behind it, and utilization becomes easier to manage. Scores typically rise steadily into the mid to high-600s with consistent behavior.

- Months 12–24: At this point, your credit history will have matured quite a bit. Scores can reach 700+, assuming no missed payments, and approval odds and credit limits will typically improve.

Timeline for rebuilding damaged credit

- Months 1–2: During these months, the focus is on stopping further damage. You'll want to bring all accounts current, set up autopay, and reduce balances where possible. Your credit score may not improve yet, but this period is super important for preventing additional negative marks.

- Months 3–6: During this period, consistent on-time payments and lower utilization begin to outweigh recent negative activity. You may start to see early score improvements, though your credit profile is still sensitive and can be set back quickly by new late payments.

- Months 6–12: Here, your recent positive behavior has enough history behind it to noticeably stabilize your score. Older negative items begin to matter less, and scores often move from poor to fair or from fair toward good with continued consistency.

- Months 12–24: At this point, your credit recovery is well established. The impact of past mistakes continues to fade, and scores can move solidly into the good range or higher, assuming no new negative activity and steady on-time payments.

How to monitor and protect your credit

If you're ready to implement all of the healthy credit habits required to build your credit, the last step is to protect your credit.

Monitoring your credit score to scout for errors and fraud is highly important so your hard work doesn't go to waste. Here are a few things to keep in mind when monitoring and protecting your credit.

Check your report for errors

Be sure to regularly review the credit report that the 3 credit bureaus (Experian, Equifax, TransUnion) maintain on you. Visit annualcreditreport.com to pull your reports 1 time per year, free of charge.[3]

Errors in credit reports are more common than you might think, and if you're applying for new credit, loans, or a job, you don't want things to ding your chances that you're not at fault for.

Dispute inaccurate information

If you do in fact find something wrong on your credit report, the next course of action is to dispute them.

You can manually send disputes to the 3 bureaus yourself, or you can use apps like Kikoff that will easily take care of the process for you.

Set up credit monitoring alerts

Several apps offer you to set monitoring alerts for suspicious credit activity, including things like:

- A new credit account or loan opened in your name

- Significant balance changes

- Changes to personal information

This lets you catch fraud early so you can avoid serious damage.

When to freeze your credit

If serious damage has occurred, such as exposure of personal information or identity theft, you can use a tool called a "credit freeze" to block any new credit accounts from being opened in your name for its duration.

This won't affect your existing credit accounts, and you can temporarily pause the freeze if you need to open a new account.

Conclusion

Taking initiative for improving credit score is as important as ever, and by utilizing the principles discussed here, you'll be well on your way to building your credit.

Be sure to adhere to best practices surrounding the 5 factors that determine your credit score, explore different methods of building credit, and monitor your credit periodically.

For an even faster boost to your credit, try out credit building apps like Kikoff, which allow you to make payments to a credit account that get reported to all 3 credit bureaus.

Finally, building credit is a very personal journey, which varies for every individual's situation. Here are few more guides to building credit if you're:

- a college student

- a U.S. immigrant

- a teenager

- recovering from bankruptcy

- recently divorced

- a retiree

- on active duty

- a military spouse

- unemployed

- a U.S. international student

- a U.S. expat

- a single parent

- a stay-at-home mom

- or a freelancer

Good luck on your credit building journey!

Frequently Asked Questions

Sources

Disclaimer: The information provided in this blog post is meant for informational purposes only and does not constitute financial advice.