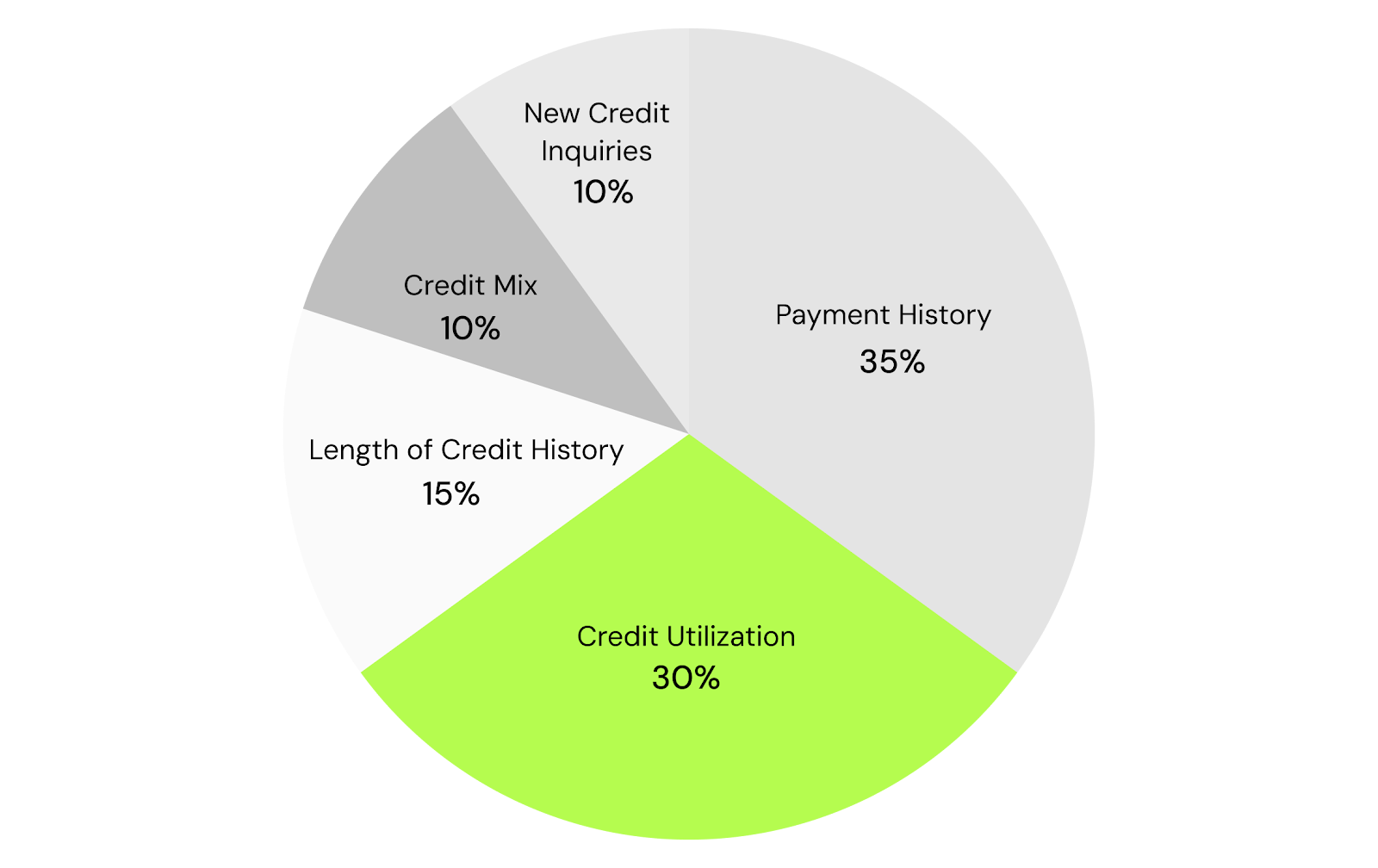

Credit utilization is an important factor that affects your credit score. In fact, it accounts for about 30% of your FICO score and roughly 20% of your VantageScore.

Credit utilization refers to the amount of credit you use compared to your total credit limit. For example, if you have a credit card with a limit of $5,000 and you have a balance of $1,000, your credit utilization rate is 20%.

Let's jump in!

What is credit utilization?

Credit Utilization is the amount of credit line you use out of your available total.

For example, if you can borrow a total of $10,000 and spend $5,000, your utilization rate will be 50%.

This percentage is based on the total number of revolving lines of credit you have, as well as each individual credit line. So what are revolving lines of credit? They're accounts where you can borrow up to a maximum limit and pay back over time, like credit cards, personal lines of credit, and home equity lines of credit.

Credit utilization vs. credit limit

Credit utilization and credit limit are closely related, but they measure very different things.

Your credit limit is the maximum amount of money that your lender allows you to borrow. For example, if you have a credit card with a $6,000 limit, you can owe up to $6,000 on that credit card at any given time.

On the other hand, credit utilization is the percentage of the credit limit that you spend.

If you spend $750 of that $6,000 credit limit, your credit utilization is 12.5%.

Credit utilization = money spent ÷ credit limit

Overall vs. per-account credit utilization

Your credit utilization ratio can come in multiple ways, not just as a single number.

Overall credit utilization reflects the average utilization across all of your accounts. If you have two accounts with a $5,000 credit limit, and one account has a credit utilization rate of 40% and the other 10%, your overall credit utilization would be 25%.

On the other hand, per-account credit utilization is just the individual credit utilization rate for each account on your report.

How does credit utilization affect your credit score?

Lenders and creditors use credit utilization as an indicator of your creditworthiness.

They want to see that you can manage credit responsibly and that you're not maxing out your credit cards or other credit accounts. A high credit utilization rate can signal that you may be a risky borrower, which could make it harder to get approved for credit in the future.

Credit utilization also makes up about 30% of your FICO credit score, making it one of the most important scoring factors. High utilization rates can hurt your credit, so the lower your utilization rate, the better.

What is a good credit utilization rate?

Generally, it's recommended that you keep your credit utilization rate below 30%. However, the lower the better.

For example, if you have a credit limit of $10,000, you should aim to keep your balance below $3,000. This shows lenders that you're responsible with credit and can manage your finances well.

If you can aim for 15% or even 10% credit utilization, you'll be in a great position to grow your credit.

What factors into your credit utilization rate?

Your credit utilization ratio is only based on revolving credit lines, such as the following:

- Credit cards (including retail and store credit cards)

- Authorized user credit cards (as long as the card's account appears on your credit report)

- Personal lines of credit

- Home equity lines of credit

- Closed revolving credit accounts that still carry a balance (even if they're rarely used)

Usually, each of these revolving credit lines report both a balance and credit limit to the bureaus, which are used to calculate your credit utilization rate.

On the other hand, non-revolving credit lines do not count towards your credit utilization rate. Examples include:

- Auto loans

- Student loans

- Mortgages

- Personal loans with fixed payments

- Buy now, pay later loans that report as installment accounts

Even if these accounts have high balances, they don't get reported as part of your credit utilization since they're not revolving.

If you find yourself with extra cash and want to improve your score, instead of paying more on your car note, use that cash to pay down your credit card.

Reported vs. real-time credit utilization

Keep in mind that your credit utilization rate is based on the balances and credit limits that appear on your credit report, not your real-time account activity.

This means that if your utilization temporarily spikes but you pay it down before your card issuer reports your balance to the credit bureaus, that spike often won't appear on your credit report or impact your reported credit utilization. Keep in mind that reporting practices can vary by issuer, so it's not guaranteed in every case.

Most lenders report balances once per billing cycle, usually on your statement closing date. Knowing this date can help you manage your balances so that your reported utilization reflects the level you want.

How to improve your credit utilization rate

If you have a high credit utilization rate, there are a few things you can do to improve it:

- Pay down your balances: The most effective way to lower your credit utilization rate is to pay down your balances. This will not only improve your credit utilization rate, but it will also reduce the amount of interest you're paying.

- Increase your credit limit: If you're not able to pay down your balances, you may want to consider asking your creditor for a credit limit increase. This will increase your available credit, which can lower your credit utilization rate.

- Use credit sparingly: Try to avoid using credit for unnecessary purchases. Only use credit when you need to and when you know you can pay it back in full.

- Become an authorized user: If you have someone in your family who has good credit habits and access to credit cards, becoming an authorized user on at least one of their cards will spread the benefits of their spending to your credit score.

- Monitor your credit utilization: Keeping an eye on your credit utilization rate can help you catch any potential problems early on. You can use a credit monitoring service to monitor your credit score and utilization rate.

Conclusion

Credit utilization is an important factor that affects your credit score. Keeping your credit utilization rate low is a key part of maintaining a healthy credit score. By following the tips above, you can improve your credit utilization rate and improve your creditworthiness over time.

If you're looking to build your credit score, sign up for Kikoff, and start building your credit for as little as $5 per month.

Frequently Asked Questions

Sources

Disclaimer: The information provided in this blog post is meant for informational purposes only and does not constitute financial advice.