Typically, a credit score above 670 is considered good, while a credit score above 740 is considered very good.

However, what is really determined as “good” depends on each lender, and what kind of credit you're applying for.

Let’s jump into some specifics.

What is a good credit score in 2026?

As mentioned earlier, a good credit score is generally anything above 670.

However, there are 2 main scoring models, FICO and VantageScore, and it’s important to understand the differences between both of them, as they vary slightly in what credit scores are considered “good”.

What is a good FICO score?

A good FICO score is anything above a 670 credit score.

This is because the base FICO score ranges from 300 to 850, with the middle range sitting at 670 to 739. So if your credit score is in that range or higher, you’re considered to have a good FICO score.

What is a good VantageScore?

VantageScore uses the same range as FICO, 300-850. However, the good range is slightly different.

A good VantageScore is anything higher than 661, since VantageScore’s “good” range is 661 to 780.

Before VantageScore 3.0 came out in March 2013, VantageScore used a different range from FICO (501 to 990), but that range is rarely used anymore. VantageScore is now on its 5.0 model, which retains that 300-850 model to be consistent with FICO.

What is a good credit score to buy a home?

To afford a home in the U.S., you’ll want at least a 670 credit score on average.

However, this is a generalization, and this will ultimately vary depending on the market, home value, and type of loan you take out.

Conventional mortgages typically require a minimum of a 620 credit score, but keep in mind - your credit score is actually a determining factor in the interest rate of your home mortgage.

If you’re looking for a FHA loan, the requirements are a bit more lenient - you can qualify with a minimum credit score of 580, with a minimum down payment of 3.5%.

So while you can assume an average “good enough” credit score to be a 670, try to factor in what you can afford to set credit building goals for yourself before you apply for a mortgage.

What is a good credit score to buy a car?

Similar to buying homes, a good credit score is really determined by how much interest you anticipate paying on your auto loan.

Also, it’s important to distinguish between new and used cars.

New cars will require you to generally have higher scores, often in the 700+ range. Used cars on the other hand can be easier to finance with lower credit scores, but again interest rates will be less favorable.

Overall, a credit score above 670 (for both FICO and VantageScore) will get you approved as a baseline for most auto loans.

What are the credit score ranges?

There are 5 standard groupings of credit scores: poor, fair, good, very good, excellent.

Excellent

Starting at the top, an excellent credit score is considered 800 to 850 (850 being the highest credit score possible)

You have to demonstrate perfect (or near perfect) credit to get up into this range, as well as a long history of good credit behavior, such as low utilization, never missing a payment, and a healthy mix of credit types.

Very good

To be in the very good credit score bucket, you’re looking at a 740-799 credit score.

Oftentimes people will be in this category if they have good credit history, but only have a few years of it. In this situation, continue maintaining your positive credit habits and watch your credit score slowly rise higher and higher over the years.

Also, many will find themselves in this category as they’re rebuilding their credit from a lower category. If this is you, keep up the good work!

Good

A “good” credit score is anything from 670 to 739.

This credit score range is usable, but in order to lock in better interest rates, you’ll want to take action to improve your credit score to get into that very good category.

Fair

A fair credit score is anything from 580-669. Many find themselves in this category if they have some combination of late payments on their credit report, high credit utilization, frequent hard inquiries, and one or a few types of credit in the mix.

Interest rates and terms tend to be quite unfavorable here, so you’ll want to take steps to improve your credit to get to the good and very good category.

Poor

A poor credit score is anything from 300 (the lowest possible score) to 579.

In this range, you’ll have trouble getting approved for most credit lines, and loan terms will be highly unfavorable.

If you’re in this range, you’ll want to take immediate action to fix your credit. Start by paying every future bill on-time (with no late payments at all), and pay off past-due accounts as soon as possible.

Start adding positive credit as well - this can be done by opening a secured credit card, or exploring credit building apps like Kikoff, which allow you to pay small monthly fees that are reported as positive credit history to the 3 bureaus.

Where does the average American sit?

About 71% of Americans have a “good” (670) or better credit score. Here is the breakdown by score range:

What information affects your credit scores

There are 5 core factors that go into both your FICO and VantageScore credit score. Let’s go through each one so you have a better idea of how to get to a good credit score.

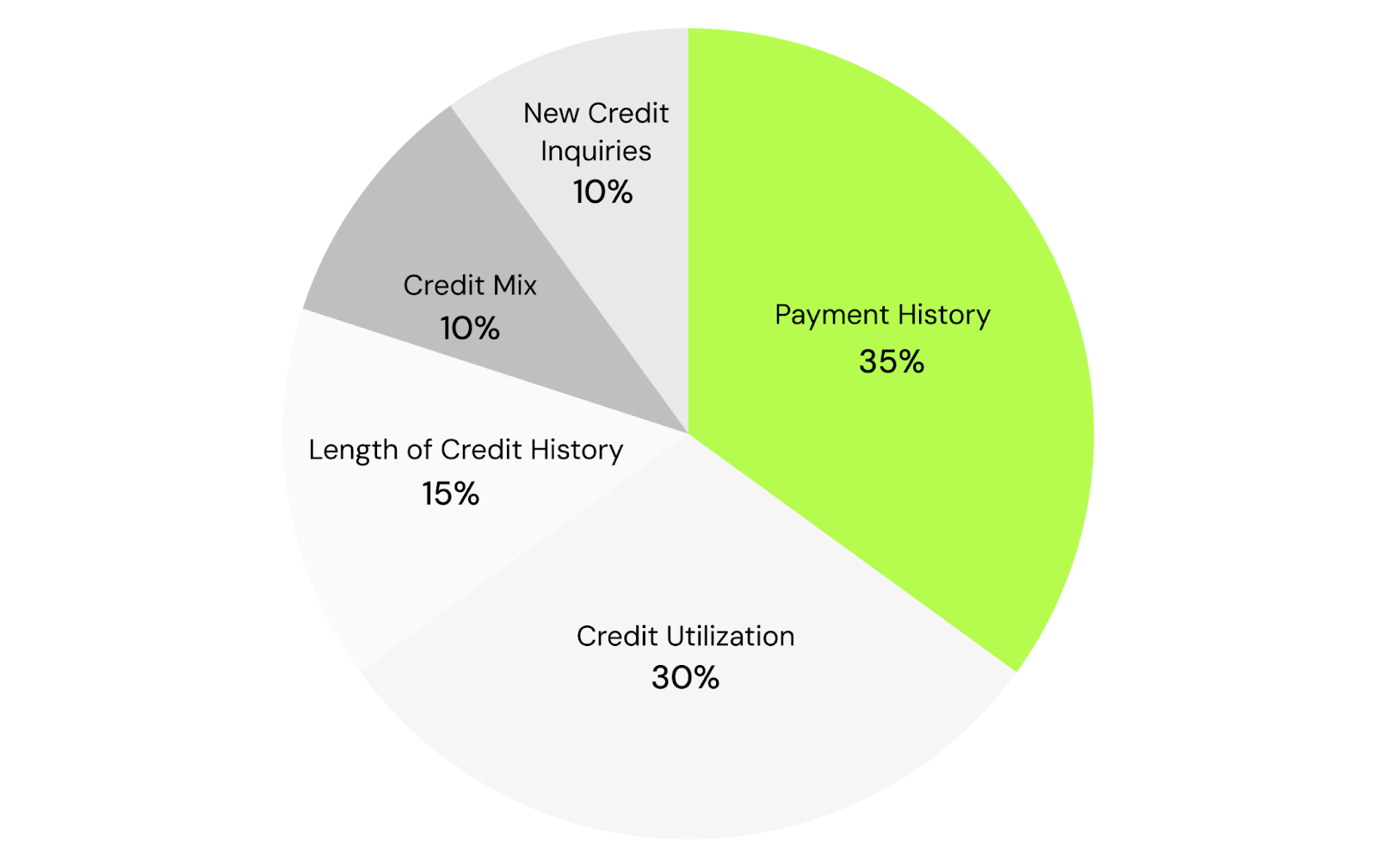

1. Payment history

Payment history is the single most important factor in determining your credit score.

This factor answers one question lenders care most about, “do you pay your bills on time?”

Payment history looks at whether each agreed payment was made on time, was late, or unpaid at all across all reported accounts, including:

- Credit cards

- Loans (auto, personal, student, mortgage)

- Credit-builder or installment accounts

- Collections tied to credit accounts

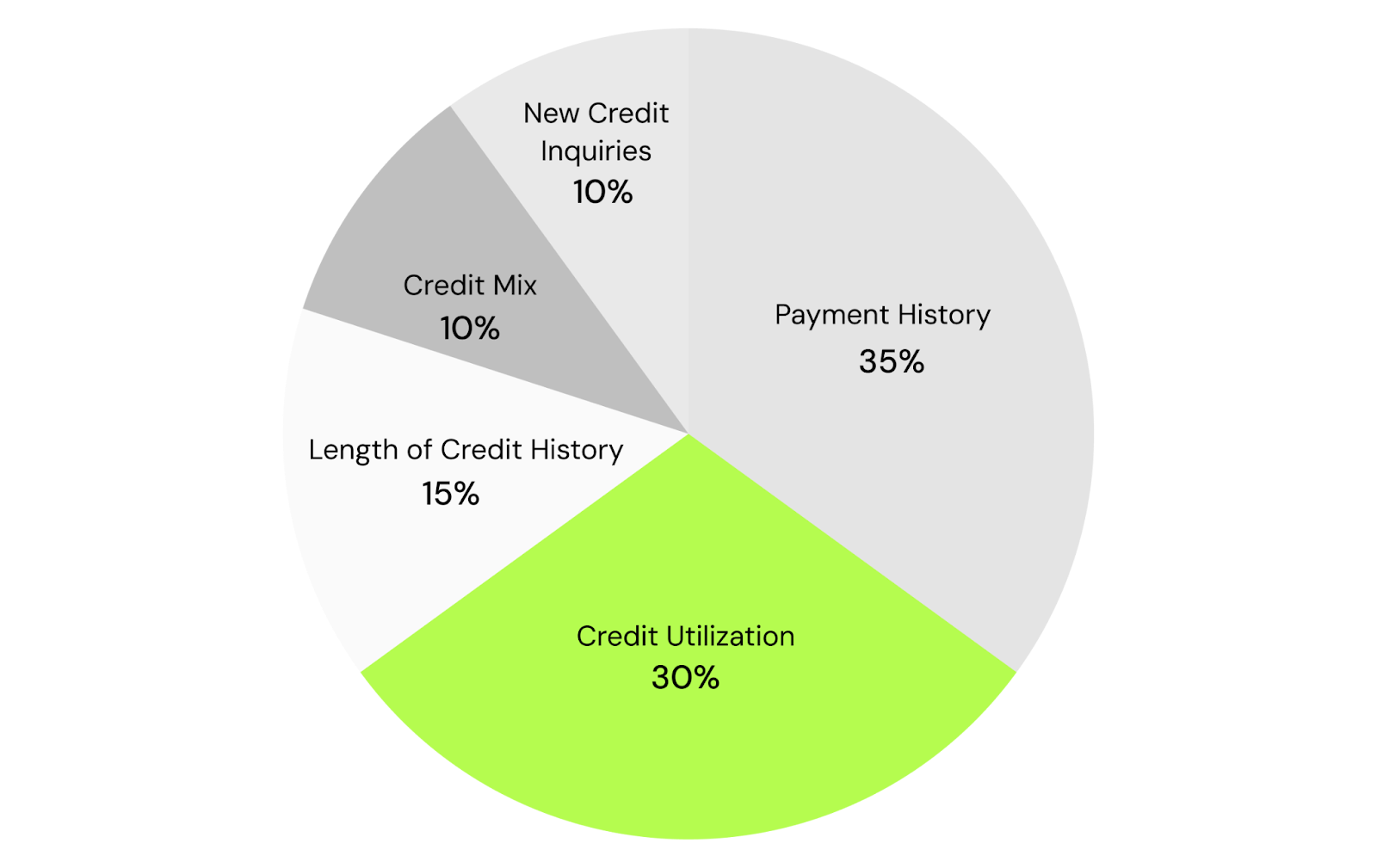

2. Credit utilization

Credit utilization measures how much of your available revolving credit you’re using.

Credit utilization mainly references revolving lines of credit, such as:

- Credit cards

- Department store cards

- Gas cards

- Secure Cards

This is basically any credit line that renews or resets periodically.

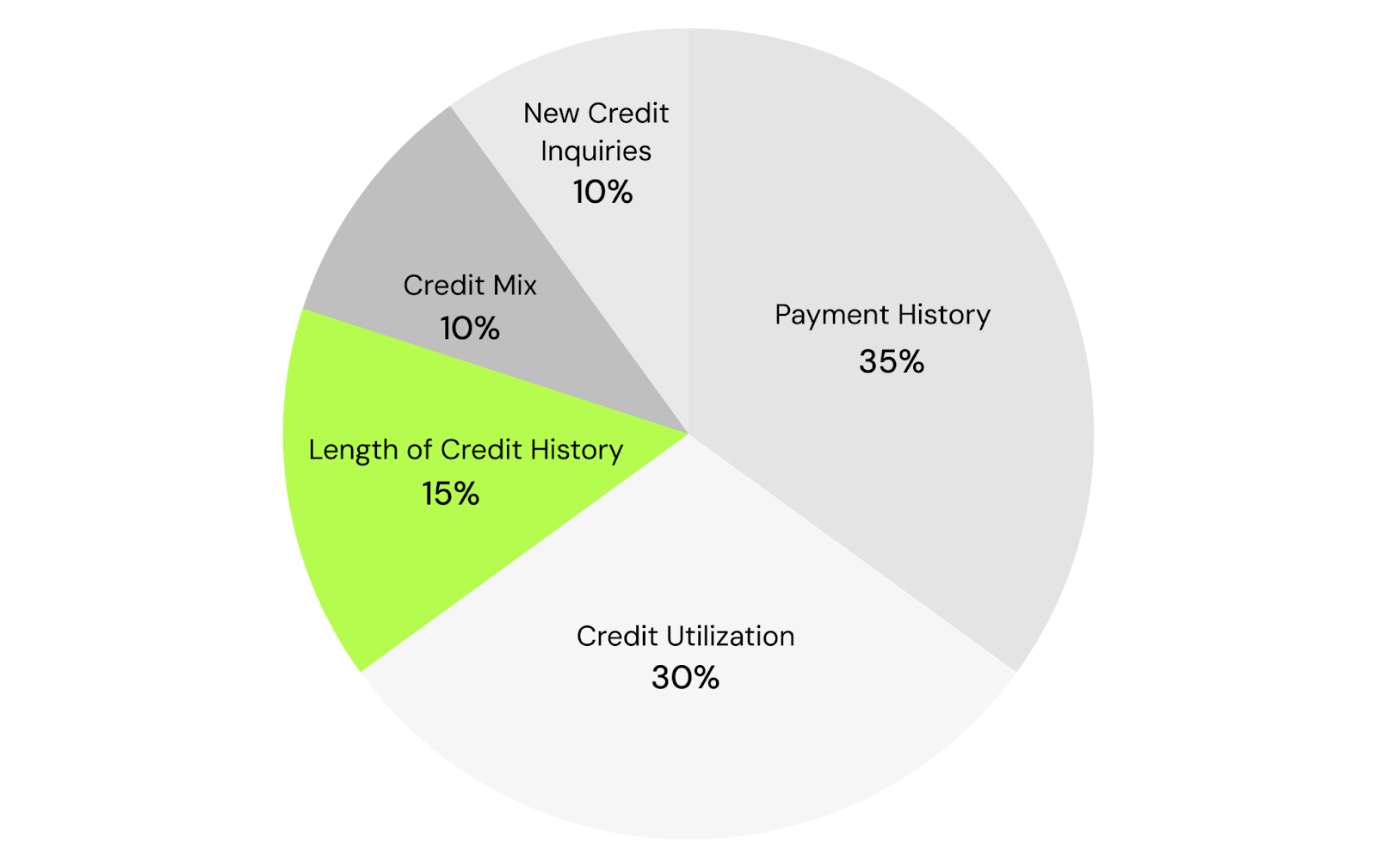

3. Length of credit history

Length of credit history is an indication of, on average, how long you’ve been using credit.

While this isn’t as impactful as credit utilization or payment history, this does set a ceiling for how high your credit score can go.

If you have a longer credit history, that is generally a positive signal, as opposed to a short credit history where lenders can’t observe your payment behavior over long periods of time.

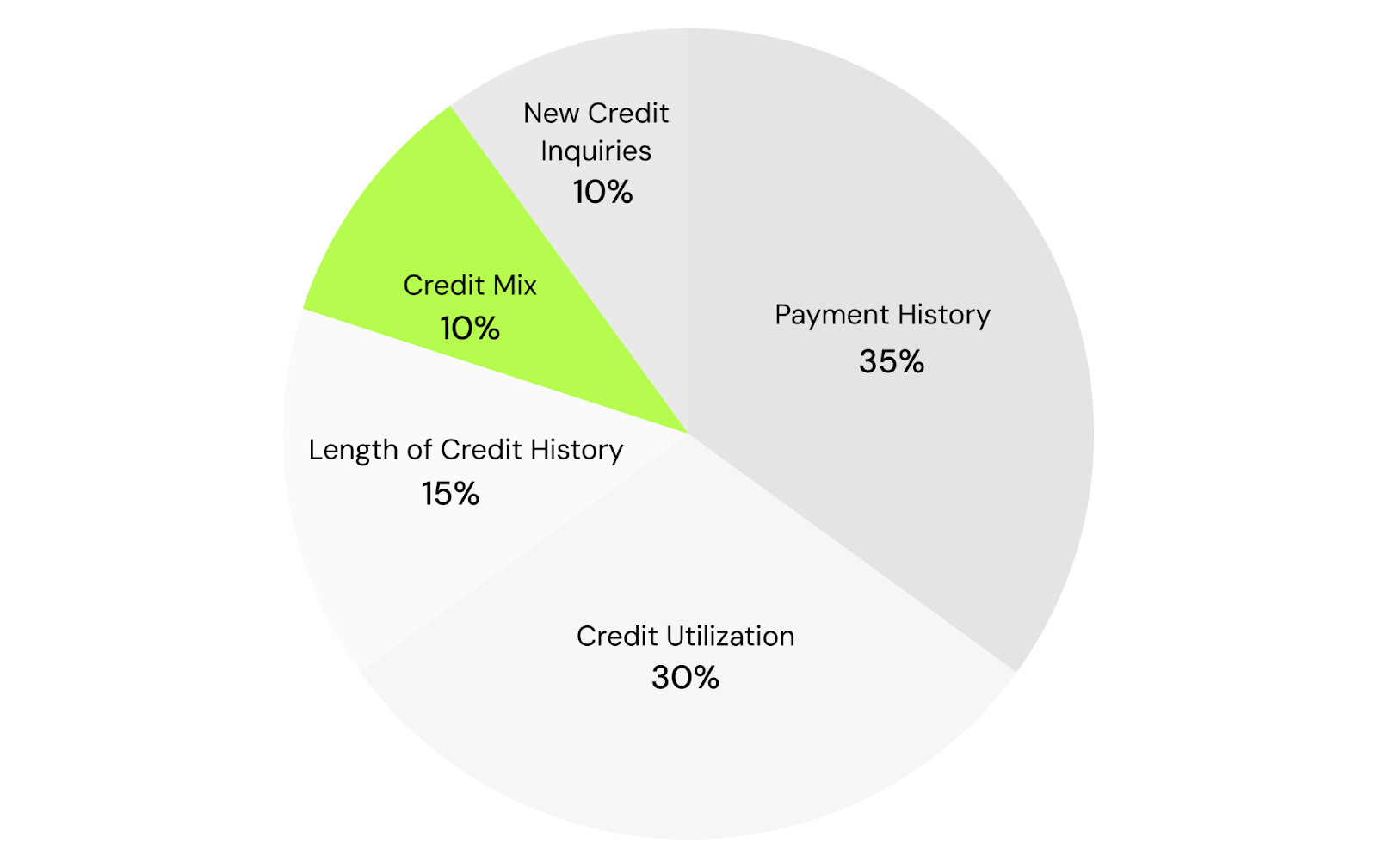

4. Credit mix

Credit mix is a measure of the variety of credit types you’ve managed.

If you’ve managed only credit cards, this is seen as a weaker credit mix than someone who has managed both credit cards and auto loans.

5. New credit inquiries

“New credit inquiries” refers to how often you apply for new credit with a hard inquiry.

You'll generally see a new inquiry on your report when you apply for:

- A new credit card

- An auto loan

- Finance accounts like a cell phone, furniture or other large purchases

Hard inquiries, a smaller factor, making up ~10% of your credit score should only be reported for 2 years and impact you for 1 year.

These 5 factors are the core of both FICO and VantageScore, but they’re calculated slightly differently.

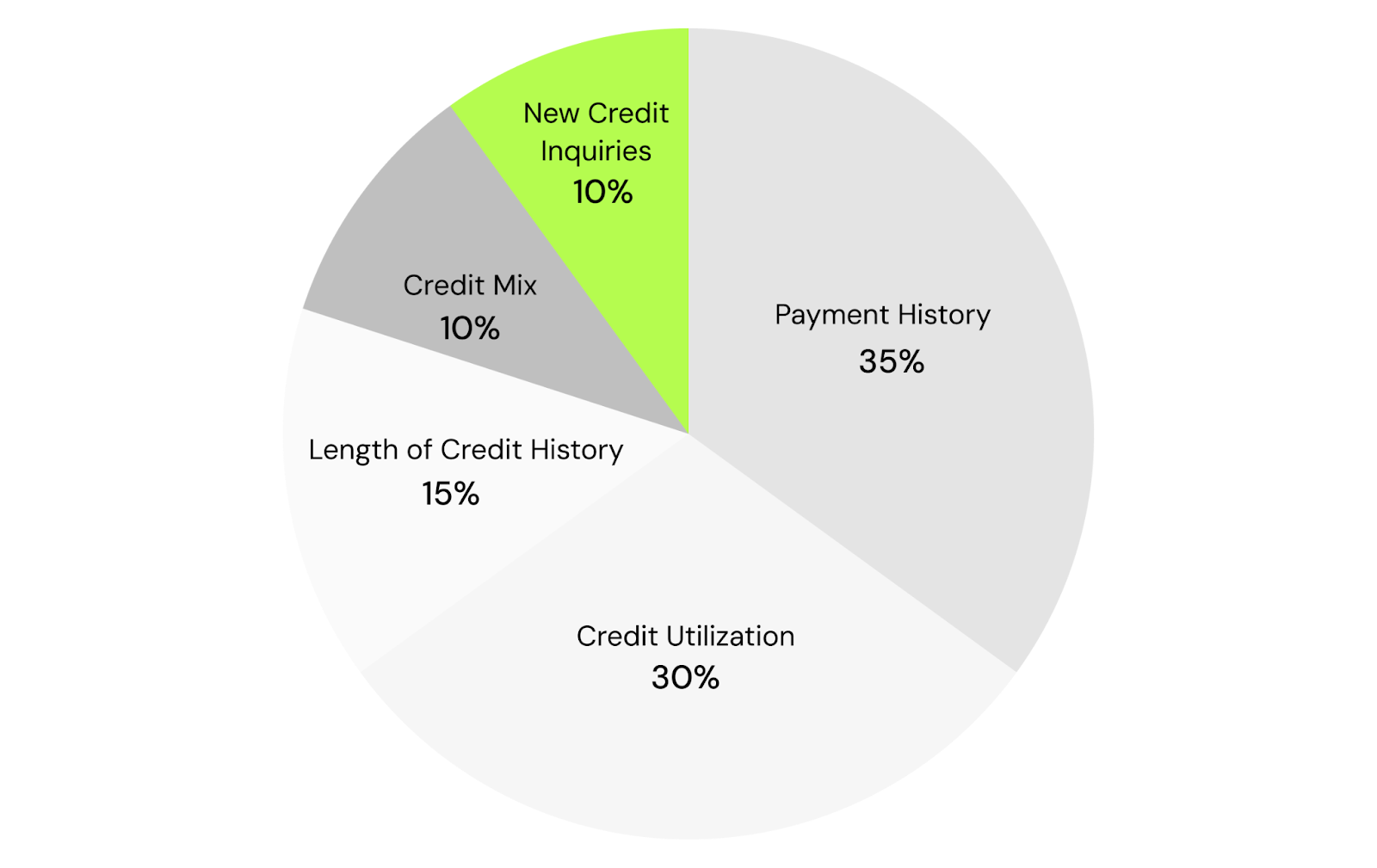

FICO score factor breakdown

FICO scores are broken down in the following percentages:

Keep in mind these are rough approximations, and the exact percentages really do depend on each individual’s credit report.

VantageScore factor breakdown

VantageScore skews similarly, but the approximate percentages differ slightly:

What information doesn’t impact your credit score

There are a lot of factors many people assume play a role in their credit score, but in reality do not.

1. Personal and demographic info

Credit score models are prohibited by law from considering any of the following factors in the calculation of your credit score:

- Age

- Race or ethnicity

- Religion

- Gender or sexual orientation

- Marital status

- National origin

- Where you live (city, state, zip code, etc)

2. Income or job details

Your credit score is in no way influenced by the amount of money you make, or any details about your employment. Whether you’re paid hourly or salary, what your job title is, none of it affects your credit score.

However, lenders may oftentimes ask you for this information when approving credit, which may influence the terms they give you, but it’s not an actual factor that goes into your credit score itself.

3. Bank account activity/spending behavior

Many people assume that the credit score models factor in your spending habits, but the reality is they don’t.

Some examples of activities that you can be rest-assured don’t affect your credit score:

- Bank account balances

- Debit card usages

- Overdrafts (unless they’re sent to collections)

- Cash deposits/withdrawals

- What you buy/where you shop (even on credit cards)

Credit scores care more about the amount of credit you’re using, and when you pay it off - not what you actually use that credit for.

How to build your credit score

To build your credit score, you’ll want to adhere to good principles surrounding the 5 factors that make up your credit score:

- Always pay your balance on time, don’t have any late payments

- Don’t utilize more than 30% of your available credit on any credit line (the lower the better)

- Leave old accounts open to increase your credit history length (the older the better)

- Strategically increase the variety of credit you have (but don’t request for new credit too often)

Several strategies can help you out here:

- Open a secured card or student credit card, don’t spend more than 15% of your credit limit, and pay it off on time, every time.

- If you’re comfortable with it, graduating to a standard credit card will push your credit score up even more if also used responsibly.

- Consider a credit building app like Kikoff, which lets you make small monthly payments which get reported to bureaus as positive payment history (the largest factor in building credit)

Why it’s important to have a good credit score

A good credit score makes your life cheaper, easier, and gives you more financial options.

First off, you will pay less for borrowed money. When you take out a loan, there is an interest rate on your loan which increases the amount you have to pay on your loan payments. If you have a higher credit score, that interest rate will be reduced - depending on the types of loans you may have, this can save you thousands or even tens of thousands of dollars in the long run.

Secondly, you’re more likely to get approved for credit cards and loans, as well as housing. It reduces the need for a co-signer or high security deposit, and gets you access to higher credit limits in general.

Having a good credit score also gives you a lot of flexibility in times of emergency. With a good credit score, you’ll be able to handle unexpected expenses without needing loans with bad terms, and you can generally gain access to credit in a pinch if needed.

And not to mention, strong financial standing brings you much more confidence and stronger mental health in your daily life.

All in all, having a good credit score signals that you’re financially reliable. This information is useful when shopping for phone plans, auto loans, applying for jobs, and other instances where demonstrating your reliability can get you to your goals.

How to monitor your credit score

If you’re making the effort to build your credit score, also be sure to know how to monitor it.

To monitor your credit score, you can either head over to annualcreditreport.com to get a credit report from each of the three bureaus (Experian, Equifax, TransUnion), or you can download an app like Kikoff or Credit Sesame to quickly monitor it for free.

annualcreditreport.com pulls your credit report directly from the bureaus, and helps you monitor your FICO score. Keep in mind, this can only be done for free once per year.

Many apps exist nowadays, like Kikoff, Credit Karma, and others, which allow you to check your VantageScore any time you want.

On top of the benefits of tracking your credit building progress, monitoring your credit is highly important for avoiding identity theft.

Credit reports tell you if a credit line has been opened in your name - if you don’t take action to look out for this kind of behavior, you can see disastrous consequences to your credit score and financial situation.

Lastly, errors can easily occur on your credit report that don’t indicate fraud, but you’ll still want to take initiative to dispute them so they don’t reflect poorly on your credit score.

Conclusion

Aiming for a good credit score is just as important in 2026 as it has always been. Try to work to get to that 670 credit score at the bare minimum, and if you can, try to push it to even the very good range, which is anything above 740.

If you’re looking for a boost to get you to that good credit score sooner, check out Kikoff, a credit building app that lets you make payments to a tradeline that gets reported as positive credit history to the bureaus.

Good luck with your credit building journey!

Frequently Asked Questions

Sources

Disclaimer: The information provided in this blog post is meant for informational purposes only and does not constitute financial advice.