.jpg)

If you've ever gotten a credit card offer in the mail, you might have noticed that it came with several pages of paperwork. As you flipped through that paperwork, you may have seen a table with several numbers in large-print font. That table is called a "Schumer box," and you should study it closely if you're thinking about taking out a credit card.

You might wonder: What is Schumer box? And why is it important? We'll take a closer look.

What is Schumer box?

A Schumer box is a table included in credit card agreements and promotional materials. Schumer boxes usually have two sections: one for interest rates and charges, and the other for fees.

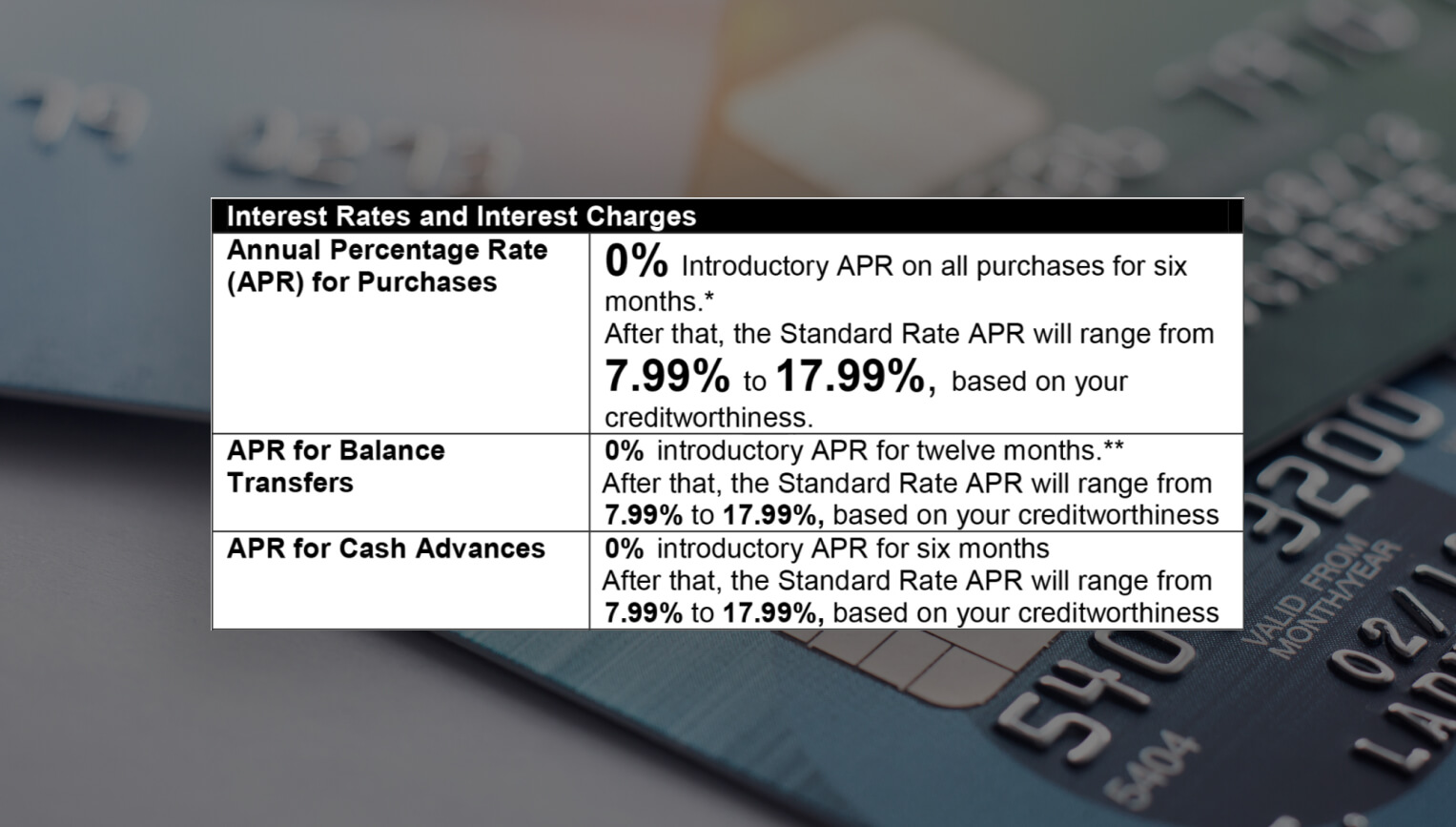

Here's what's usually included in the interest rates and charges section:

- Annual percentage rate (APR) for purchases

- APRs for cash advances and balance transfers

- Penalty APRs

- When interest accrues and when you'll be charged for it

The fees section can include the following:

- Annual fees

- Transaction fees

- Balance transfer fees

- Cash advance fees

- Late payment fees

- Foreign transaction fees

- Late payment grace periods

Schumer boxes usually include a link to a Consumer Financial Protection Bureau (CFPB) webpage with more information about choosing a credit card.

Why the Schumer box was created

What is Schumer box for? It was created to protect consumers from hidden fees and make it easier for them to compare credit card agreements.

The box was named for New York Senator Chuck Schumer, who supported legislation to make credit card terms easier for applicants to understand.

How to read and understand a Schumer box

Here's a closer look at key features of the Schumer box and what they mean.

Annual percentage rates

The APR is the interest rate you'll owe if you don't pay your statement balance in full. For cards with 0% introductory APRs, there should also be details on how long the offer will last.

The interest rates and charges section must include information about any other applicable APRs. Many cards have separate APRs for cash advances and balance transfers, for example. Lenders may also charge higher penalty APRs if you miss a payment.

Fees

Not all cards charge an annual fee, but if yours does, it must be included in the Schumer box. The fee section must also explain cash advance fees, which are often charged in addition to cash advance APRs. This fee is typically 3% to 5% of the amount of cash withdrawn.

Other fees may include balance transfer fees (usually 3% to 5% of the transferred amount) and fees for late payments. Some cards will also charge an additional fee for foreign transactions.

Lastly, most card issuers will charge a returned payment fee if your bank account has insufficient funds to pay your balance.

Minimum finance charges

Minimum finance charges (or minimum interest charges) are the minimum you'll be charged each month if your card carries a balance.

Grace periods

Some credit card issuers offer a grace period. This is a window of time between the end of your billing statement and your payment due date. If you pay the statement balance before the due date, you won't be charged additional interest.

How the Schumer box relates to the Truth in Lending Act

The Schumer box was passed as an amendment to the Truth in Lending Act (TILA) of 1968. The TILA aims to protect consumers from deceptive lending practices. Specifically, it requires lenders to disclose the terms and costs of credit.

The TILA was a step in the right direction. However, the original act didn't require lenders to prominently display this information. It was often buried in pages of fine print.

Financial language can be intimidating. Before the Schumer box rule, many people still didn't understand what they were signing up for when they took out credit cards.

By the year 2000, credit card companies were required to include Schumer boxes on credit card paperwork. This was a victory for consumers in many ways:

- It established a standardized format so consumers could easily compare rates across cards

- It required larger font sizes to make important information easier to read

- It required lenders to use a table format that made it easily recognizable

The law requires the purchase APR, which is one of the most important considerations when getting a credit card, to be displayed in at least an 18-point font.

Most other terms must be in a 10- to 12-point font. To put that in perspective, the fine print on credit card agreements and similar documents is often in a 6-point font.

Conclusion

Schumer boxes can help you make an informed decision when choosing a credit card. But in a world where credit card companies and other lenders compete for your money, it can be helpful to have a financial ally.

That's why we're here. At Kikoff, we work with people with poor or no credit to help them build their credit scores and become financially empowered. The way it works is simple. Once you sign up and get approved, we give you a small credit line that you can use to purchase items from our in-app store. You then make interest-free payments on your purchases, and we report those payments to credit bureaus.

If you're thinking about starting your credit-building journey, open an account with us today!

Frequently Asked Questions

Sources

About the editor

Disclaimer: The information provided in this blog post is meant for informational purposes only and does not constitute financial advice.