.jpg)

The history of redlining includes one of the most consequential chapters in American housing and financial policy.

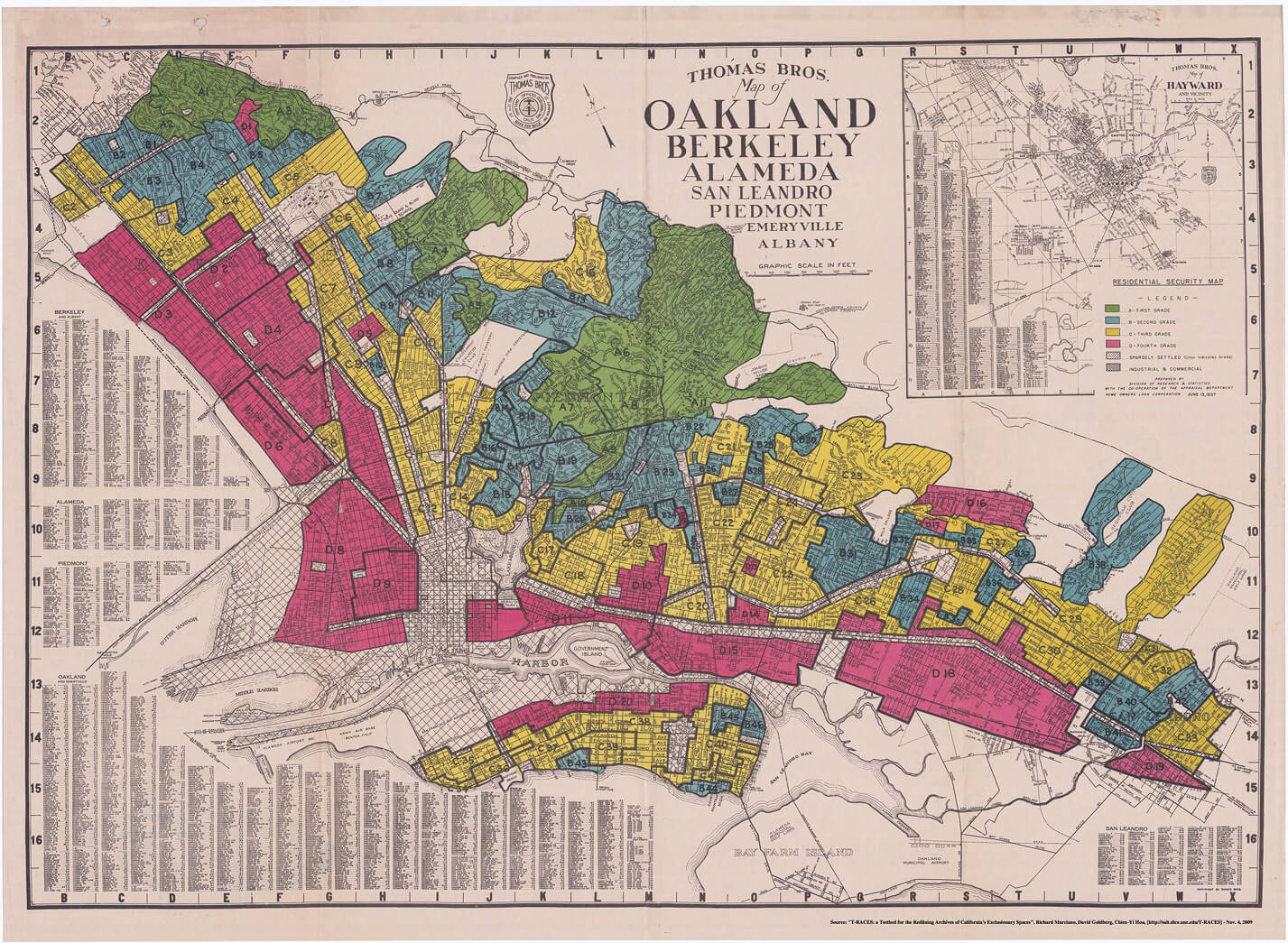

In the 1930s, a government agency graded hundreds of neighborhoods across the country to help lenders determine how risky it was to issue mortgages in each area. The agency assigned a letter grade to each area, designating the highest risk neighborhoods with red.

Unfortunately, racial discrimination was used in the map-making process. Black and other minority families had less access to mortgages, which limited their ability to build wealth through homeownership.

Although redlining was formally outlawed decades ago, its effects can still be felt in the housing market. Many communities that were denied these opportunities during the twentieth century still experience lower home values and reduced access to mainstream financial support.

Explore redlining effects on wealth and homeownership, as well as recent efforts aimed at addressing the credit access gap to promote greater equity.

What was redlining?

Redlining refers to the systemic denial of financial products, particularly mortgages, to residents of certain neighborhoods based largely on racial or ethnic composition. The practice became embedded in federal housing policy during the New Deal era and remained influential for decades.

At the time, lenders claimed that they were using legitimate criteria to evaluate the risk of borrowers and denied them purely on those factors. The reality is that many lenders made discriminatory assumptions about race and neighborhood demographics. Areas with higher black populations were routinely labeled as being too risky to lend to.

The Home Owners’ Loan Corporation and the origins of the practice

The Home Owners’ Loan Corporation (HOLC) was established in 1933 and represents the clearest beginning of the history of modern redlining. [1] Lawmakers formed the HOLC to help homeowners by refinancing mortgages and stabilizing the housing market.

The HOLC worked closely with local real estate professionals and appraisers to evaluate neighborhoods across the country. The HOLC used these partnerships to create detailed maps that classified residential areas based on risk.

For the next several decades, lenders across the country used these maps to guide their lending practices. That’s where the history of redlining began.

How neighborhoods were graded and what the maps actually showed

The HOLC used a four-tier grading system, ranging from A to D. The zones were as follows:

- A (Best): These areas were coded in green and were always upper or upper-middle-class white neighborhoods

- B (Still Desirable): Coded in blue, these neighborhoods were generally mostly or completely white.

- C (Declining): Coded in yellow and composed of working-class or first/second-generation immigrants from Europe

- D (Hazardous): D zones were literally coded in red and typically received this grade because they were “infiltrated” by “undesirable populations,” such as black, Mexican, Asian, or Jewish families

The practice eventually became known as redlining because the lowest-rated neighborhoods were coded in red.

The role of the Federal Housing Administration in institutionalizing redlining

The FHA was established in 1934 and helped transform housing finance in the United States by facilitating long-term, low-down-payment mortgages.

However, FHA underwriting guidelines reflected many of the same biases embedded in the HOLC maps. The agency prompted lending in racially homogenous neighborhoods and frequently treated racial integration as a potential risk factor.

These discriminatory practices became institutionalized as lenders adopted FHA standards. Banks and mortgage providers often refused loans in minority neighborhoods or offered less favorable terms.

How redlining shaped wealth and homeownership in America

Homeownership has long been one of the primary methods through which American families build wealth. Redlining prevented millions of households from participating fully in this wealth-building process.

The consequences of redlining extend well beyond housing. Those who were denied access to home loans also lost out on the equity that came with it, which impacted their educational opportunities and retirement security.

The postwar housing boom and who was excluded from it

The United States experienced one of the largest housing booms in history. Federal mortgage programs and rapid suburban development helped millions of families purchase homes.

Many black families were largely excluded from these opportunities. Mortgage financing that was readily available in white suburban communities often remained inaccessible in minority neighborhoods.

White families benefited from the appreciation of their homes and equity accumulation. These gains became an important source of generational wealth.

Blockbusting, contract buying, and the predatory alternatives to mortgage credit

The lack of access to traditional home loans left minority families with few options, which led many to turn to contract buying. The contract buying process works similarly to a mortgage. A person would make installment payments on a home. When they made their final payment, they owned the home free and clear.

The catch is that contract buyers didn’t build equity like a homeowner does in a traditional mortgage. If the consumer missed too many payments, the owner could evict them, and they would lose any equity in the home.

Blockbusing was another predatory practice. Real estate agents would exploit people’s racial fears to encourage white homeowners to sell quickly at reduced prices. Properties were then resold to black families at inflated prices.

The compounding effect of denied homeownership on generational wealth

When families own appreciating assets such as homes, they can borrow against the equity, fund education, support entrepreneurship, and transfer wealth to their children. Families who were excluded from homeownership lost access to these opportunities.

Over multiple generations, even modest differences in homeownership rates can produce substantial disparities in net worth. The disparities in homeownership rates between black and white Americans are not modest.

According to the Urban Institute, 65% of white Americans owned homes, and just 38% of black Americans owned homes. [2] In 2017, the rate of black homeownership was 42%, and the rate of white homeownership was 72%.

The legal dismantling of redlining

Lawmakers began addressing discrimination in housing and lending in response to civil rights activism in the 1960s and 1970s. A series of federal laws was implemented to eliminate barriers that had excluded minority communities from equal access to credit.

Several key laws were involved in dismantling redlining. [3]

The Fair Housing Act of 1968

The Fair Housing Act prohibited discrimination in the sale, rental, and financing of housing based on race, color, religion, or national origin. Lawmakers took a huge step toward making redlining illegal with the passage of this act, although there was plenty of work to do in subsequent years.

The Equal Credit Opportunity Act of 1974

The Equal Credit Opportunity Act (ECOA) expanded protections by prohibiting discrimination in credit transactions.

Lenders could no longer legally deny loans or impose different terms based on characteristics such as race, sex, religion, national origin, age, or marital status. The law helped establish a framework for fair lending that remains central to financial regulation today.

The Home Mortgage Disclosure Act of 1975

The Home Mortgage Disclosure Act (HMDA) increased transparency by requiring many lenders to report mortgage application and approval data. Researchers, regulators, and community organizations gained access to information that could reveal patterns of discrimination and unequal lending practices.

The Community Reinvestment Act of 1977

The Community Reinvestment Act (CRA) encouraged banks to meet the credit needs of all communities within their service areas. Federal regulators evaluate banks’ performance under CRA requirements when considering mergers or other business activities. The law aimed to expand access to credit in historically underserved areas.

Why legislation alone did not end discriminatory lending

Lenders mostly complied with the provisions of these laws, but many turned to other discriminatory practices that were more subtle. Undoing the impacts of redlining and other discriminatory lending took decades.

Redlining’s legacy in modern credit access

Lenders don’t use redlined maps anymore, but many of the communities that were impacted by discriminatory lending policies still have less access to credit compared to primarily white neighborhoods.

Persistent racial gaps in mortgage approval rates

While factors such as income and debt levels are the primary variables that influence lending decisions, researchers continue examining whether historical patterns of disadvantage contribute to these disparities. The persistence of approval gaps suggests that unequal access to credit remains an important policy issue.

Concentrated poverty and the credit desert problem

Many formerly redlined neighborhoods experience limited access to traditional banking services. Communities with fewer bank branches often rely more heavily on alternative financial services such as payday lenders, check cashers, and high-cost installment loans.

These credit deserts can increase the cost of borrowing and make accumulating wealth more difficult.

How historical redlining maps correlate with credit scores and wealth today

Historic HOLC grades can still be linked back with economic indicators today. Neighborhoods that received favorable grades tend to have higher property values and greater homeownership rates. The average credit scores of individuals in these areas also tend to be on the higher side.

Conversely, areas that were redlined in the 1930s frequently show lower wealth levels and higher rates of financial distress. These findings suggest that the policies implemented nearly a hundred years ago continue to influence economic outcomes.

According to the Urban Institute, there is still a huge disparity in denial rates along racial and ethnic lines. Here is a breakdown of mortgage denial rates by race and ethnicity in 2020: [4]

Modern forms of lending discrimination

Redlining is illegal, or at least the overt form of it. However, there are many who are concerned with newer forms of discrimination that may produce unequal outcomes.

Algorithmic lending and the risk of encoded bias

Many lenders now use automated underwriting systems and machine learning models to evaluate applicants’ creditworthiness. While these systems make the lending process more efficient and reduce the role of human subjectivity, they can also convey biases if the algorithms are trained on biased data.

Lenders that use algorithms to assist with lending decisions must carefully vet the technology to identify and eliminate potential bias.

Reverse redlining and the targeting of minority communities with high-cost loans

In the late 20th century, lenders used an inverted approach known as reverse redlining. Instead of avoiding minority neighborhoods based on the idea that they were high risk, lenders targeted them with financial products. Unfortunately, the loans and financial products usually carried predatory terms.

Recent fair lending enforcement actions by the DOJ and CFPB

Unfortunately, the history of redlining is still being written, with new violations being uncovered and addressed on an ongoing basis. According to a release from the DOJ, the CFPB and OCC resolved lending discrimination claims against Trustmark National Bank in late 2021. [5] The proposed consent order included the following stipulations:

- Trustmark will invest $3.85 million toward loan subsidies for current and future residents of predominantly Hispanic and black neighborhoods in Memphis

- The bank will devote $400,000 to community partnerships

- Trustmark will allocate at least $200,000 annually in advertising to outreach, credit repair, and consumer financial education in Memphis

- Trustmark will pay $5 million in combined civil penalties to the OCC and CFPB

In August 2021, the DOJ also reached a redlining settlement with Cadence Bank. The bank was required to invest more than $5.5 million to provide more credit opportunities for residents of majority Hispanic and black neighborhoods in Houston.

In late 2015, New Jersey-based Hudson City Savings Bank agreed to a $33 million settlement to address allegations of redlining. The bank was accused of turning away Hispanics and blacks seeking mortgages. It was the largest redlining settlement case in history. [6] Of that amount, $25 million was assigned to a subsidy fund.

Efforts to close the credit access gap

Over the last several years, policymakers, lenders, and community organizations have collaborated to close the credit access gap. While there is much work to be done, these groups have made some notable progress.

Community development financial institutions and their role

Community development financial institutions (CDFIs) provide loans and financial services in underserved communities. These organizations prioritize borrowers who may struggle to obtain financing from traditional institutions while adhering to responsible lending practices.

Unlike businesses that engage in reverse redlining, CDFIs bring legitimate and equitable financial products to minority communities. They also offer financial education opportunities, which help promote personal agency. CDFIs have become important tools for promoting economic development and financial inclusion.

Alternative credit data and expanding who gets scored

For decades, individuals who use traditional credit products and own homes have been at an advantage when it comes to building credit. Homeowners get credit for making on-time payments, which is one of the most heavily weighted factors used by most scoring systems.

Recently, non-traditional reporting tools have made it possible for underserved individuals and those with thin or rebuilding credit profiles to build a positive payment history. For example, consumers can report on-time rent and utility payments to contribute to their credit profile.

What equitable credit access could mean for the racial wealth gap

Homeownership rates between black and white Americans are one of the biggest sources of disparity. Promoting greater access to affordable credit can help support homeownership and asset building.

Reducing barriers to credit may help narrow wealth disparities that have accumulated over generations. However, it will likely take many years for the financial ecosystem to correct itself, even with plenty of support.

FAQ

What is redlining?

Redlining was a discriminatory practice in which lenders denied mortgages and other financial products to residents of certain neighborhoods. These policies were often based on race or ethnicity. The term comes from maps that outlined supposedly risky neighborhoods in red.

Is redlining still legal?

Redlining was made illegal through laws such as the Equal Credit Opportunity Act and Fair Housing Act. However, there is concern that modern lending systems produce outcomes that reflect the legacy of past discrimination.

What is reverse redlining?

Reverse redlining occurs when lenders target minority communities with high-cost or predatory loan products. Rather than denying credit altogether, offenders offer credit under terms that are far more expensive or risky than necessary.

Redlining and credit access as a path to equity

The history of redlining reveals how housing policy, financial institutions, and discriminatory assumptions combined to shape opportunities for millions of Americans. For decades, minority communities faced barriers to mortgage lending and homeownership that limited wealth creation and reinforced segregation.

Major civil rights laws dismantled the foundations of redlining in the 1960s. However, many of its effects remain visible in patterns of homeownership and mortgage approval rates. There are strong links between the history of redlining and present-day economic disparities among various ethnic and racial groups.

Redlining and credit access are essential elements for evaluating current lending practices and developing solutions that promote financial inclusion. The lessons learned from redlining remain relevant to those who are pursuing economic opportunity and fairness in America.

Frequently Asked Questions

Sources

- https://scalar.usc.edu/hc/jewish-histories-boyle-heights/the-home-owners-loan-corporation-and-the-redlining-of-boyle-heights

- https://www.urban.org/policy-centers/housing-finance-policy-center/projects/reducing-racial-homeownership-gap

- https://www.law.cornell.edu/wex/redlining

- https://www.urban.org/urban-wire/what-different-denial-rates-can-tell-us-about-racial-disparities-mortgage-market

- https://www.justice.gov/archives/opa/pr/justice-department-announces-new-initiative-combat-redlining

- https://www.courthousenews.com/bank-settles-landmark-redlining-action/

About the editor

Disclaimer: The information provided in this blog post is meant for informational purposes only and does not constitute financial advice.